South Africa's concerning decline in investment

South Africa's concerning decline in investment

South Africa's investment is far from its 2015 peak. What does this mean?

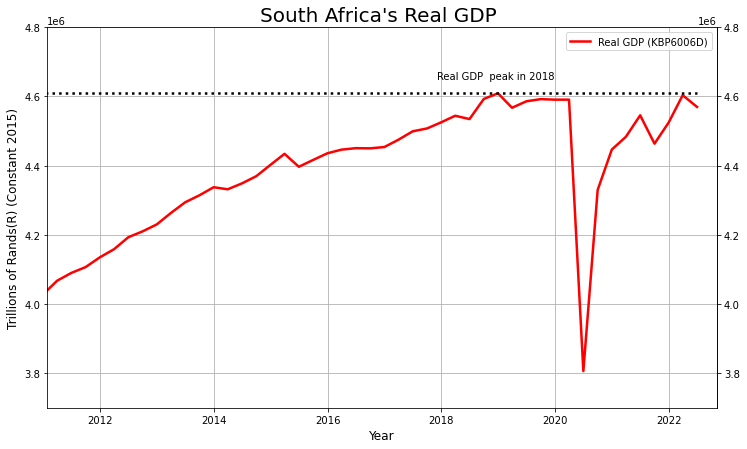

South Africa is in desperate need of investment — from residential housing, electricity, public transport, road infrastructure and other industries. The graph below illustrates how South Africa’s economic output has stalled, despite an increasing population.

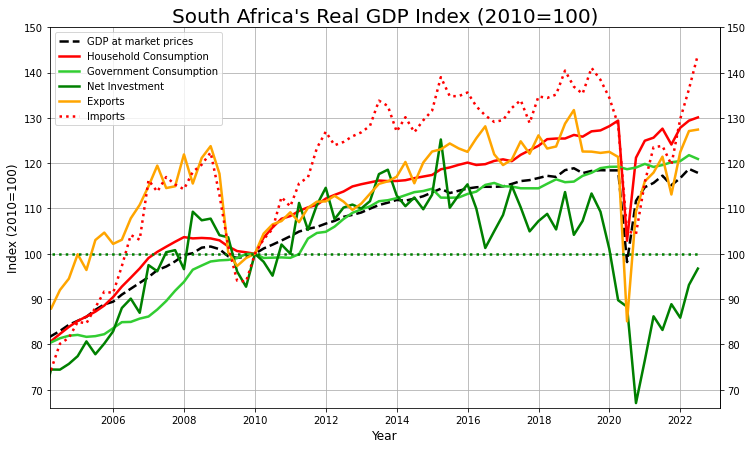

South Africa’s real GDP has not surpassed the peak in the 4th quarter of 2018 at about R4.6 trillion in constant 2015 Rands. There are multiple ways to measure GDP. One way is through the expenditure approach, in which GDP is the sum of household consumption (C), investment (I), government consumption (G) and net exports (X – M).

The graph above shows South Africa’s GDP based on the expenditure approach. What is noticeable is the importance of household consumption as a driver of South Africa's economic output. South Africa also has a high degree of trade openness, with exports and imports playing a key role. Also noticeable is the extent to which “Net Investment”1 has declined from its peak in the first quarter of 2015. This real decline is from a peak of about R850 billion to R550 billion in the most recent quarter. Note that when using the term ‘investment’, I generally refer to an increase in the gross fixed capital stock.

The decline in net investment is more evident when using an index with 2010 as the base year. Investment is the only component of GDP that is below the level it was in 2010. South Africa’s economic growth over the past decade has been reliant on Household consumption and public debt funded Government consumption. While consumption is vital for short term growth, as it increases the overall aggregate demand in the economy. Long term growth requires some sort of investment to improve the overall capacity or aggregate supply. Increased investment also increases aggregate demand, and the recent relative lack of it has seriously limited South Africa’s recovery from Covid-19 recession.

Why is investment important?

In the post about the economic growth of the Soviet Union, I emphasized the role of capital accumulation and the ‘extensive growth model’ in its industrialization. China has also made use of this investment heavy growth model. For developing countries, the value of additional investment is incredibly useful — also understood as having a high marginal product of capital. Thus, a developing country which invests a large amount of capital, should see a large increase in economic output and eventually converge with developed economies. This is one of the implications of the Solow Growth model.

The lesson of the Soviet Union is that relying on investment for growth eventually becomes less useful — there are only so many houses, factories, and bridges that one can build. The cost of capital depreciation also increases as the overall capital stock builds up. As a developing economy eventually reaches the natural limit of capital accumulation, a shift towards Schumpeterian ‘creative destruction’ driven by competition and innovation is required to drive economic growth.

South Africa is likely far from the point at which the return from investments has declined. Increased investment in cities, rural areas and townships could be incredibly useful. Electricity production is currently insufficient to meet demand, factories are required to create more jobs. Millions of South Africans lack basic housing, piped water, decent public transport, and generally decent infrastructure.

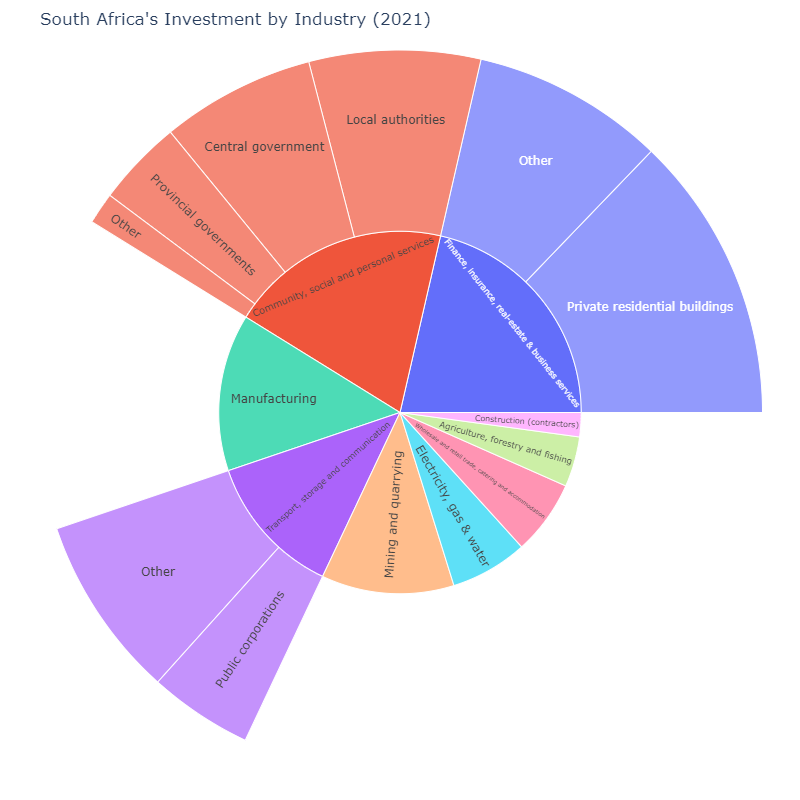

South Africa’s investment by industry

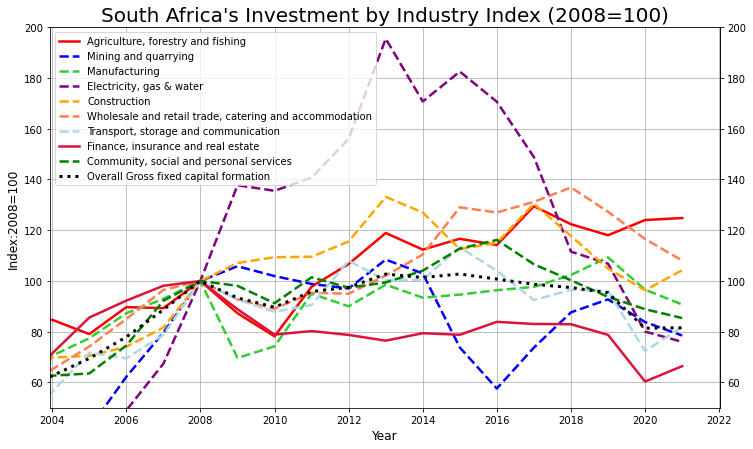

Disaggregating investment by industry reveals some interesting trends. It seems like for every industry, the peak in real investment was in the past. The finance, community services and electricity industries all seem to have significant declines from their peak. While real investment in agriculture peaked in the 1980s. Investment in electricity, gas and water has declined by more than half from its peak, from R112 billion in 2013 to R43 billion in 2021. This decline is incredible given South Africa’s current issues with electricity production.

Using an index with 2008 as a baseline, it becomes more apparent that investment has declined across almost every industry since 2008. The exceptions are agriculture, retail and construction. Electricity, gas and water saw a large increase in investment around 2013. This was likely driven by investment by Eskom for its new power stations. These have been found to be malinvestments, with vast amounts wasted to poor planning and corruption.

Despite the vast spending in electricity investment, South Africa’s overall production in electricity has declined in the 2010s. This shows that not only the amount, but also that the quality of investment is vital.

Separating investment by industry shows that private residential building forms a large component. This is also true for investment by local government and national government.

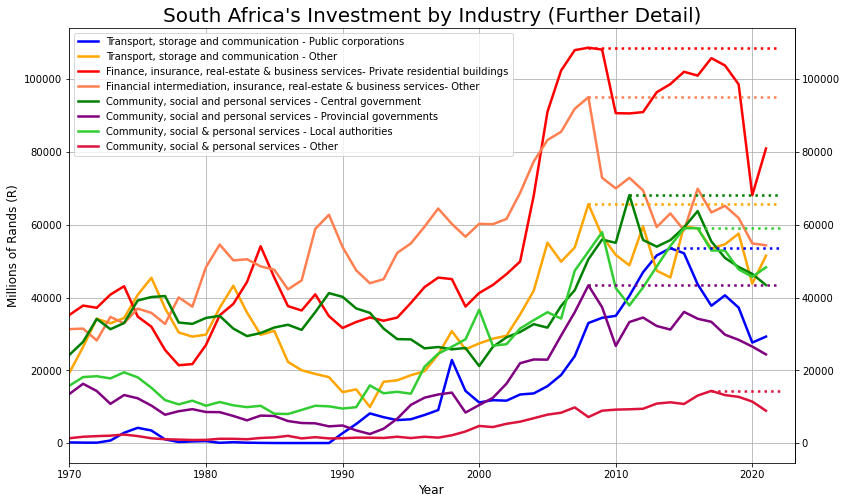

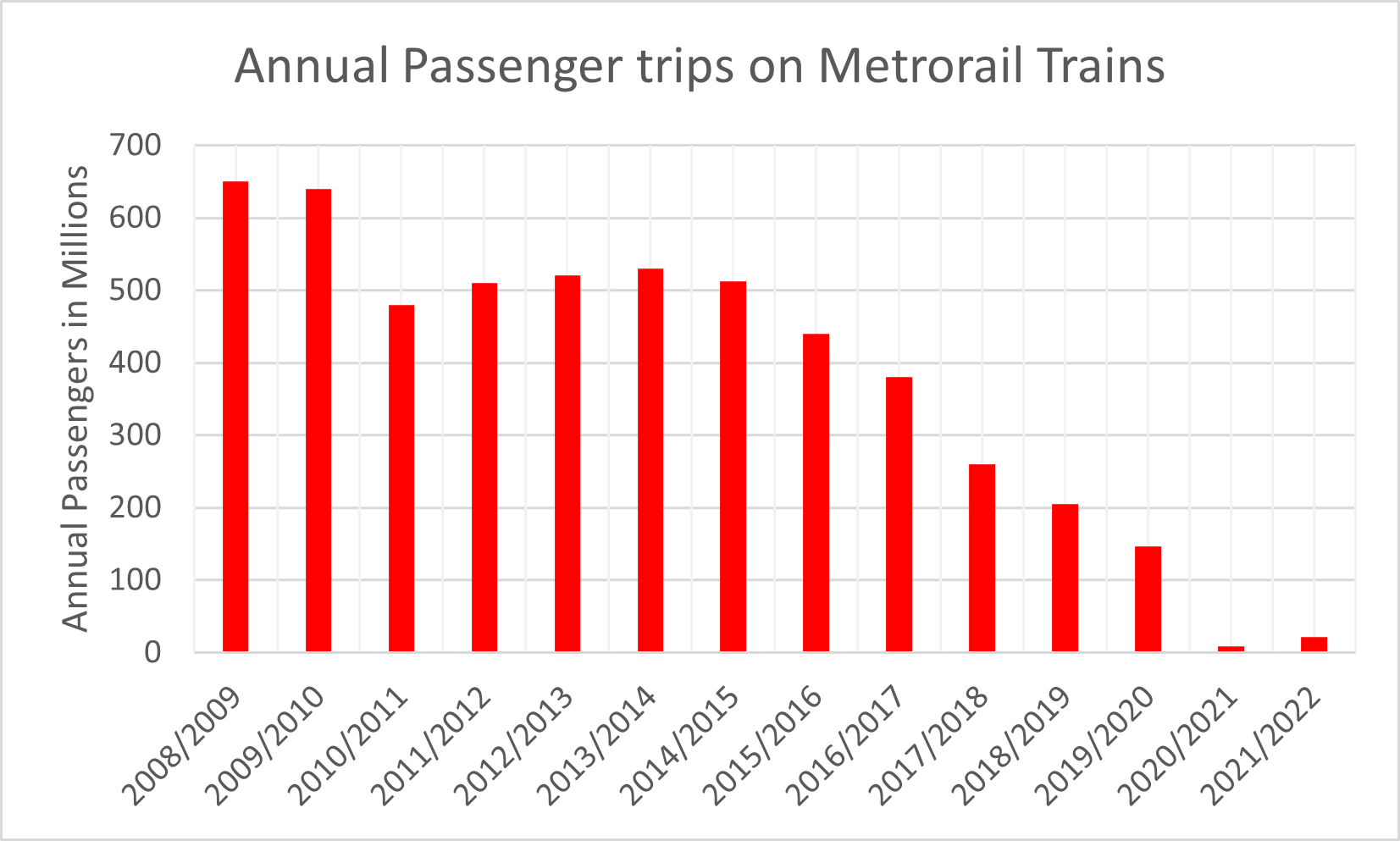

Further detail of the three largest industries by investment shows a general decline from the peak around 2008. ‘Private residential buildings’ has seen a large decline in the last two years. Since 2008 almost all subcomponents of the three industries have declined, apart from private investment in ‘Community, social and personal Services’. The significant increase and subsequent decline in ‘Public corporation’ investment in transport from R54 billion in 2014, to the is the most recent R30 billion is also noticeable. This is due to investments by Transnet, the state-owned railways company. Despite this large increase in public transport investment, the number of passengers using Metrorail trains has collapsed in the past decade.

Again, the importance of the quality of investment is evident.

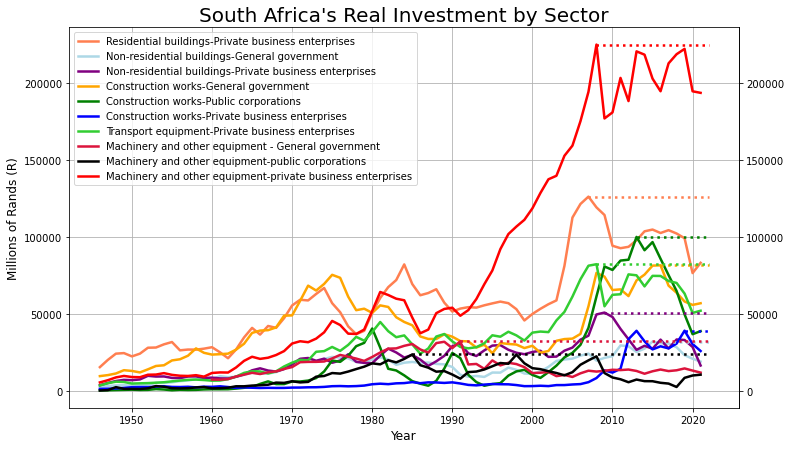

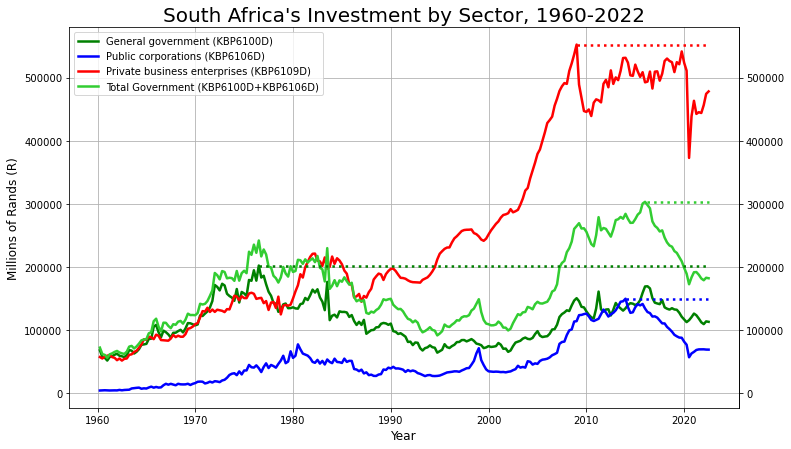

South Africa’s Investment by Sector

South Africa’s investment can also be broken down by sector. The above chart shows that most investment in 2021 was in the private sector, mostly focused on residential buildings and machinery. While public investment is geared towards “Construction works”.

South Africa’s real investment by sector over time has a similar story to investment by industry, which is that the peak in real investment was in the past. Private investment in machinery was not always the primary form investment; private residential buildings had this role in the 1980s. It is remarkable that general government investment in “Construction Works” was the primary form of investment in the 1970s.

Comparing total investment of the public and private sector over the past 60 years reveals a few interesting trends. Investment by the ‘General Government’ peaked in the 1970s — nearly all of South Africa’s freeways were built in this decade. While private investment peaked in 2008. Total public investment was mostly higher than private investment before the 1990s. Investment by ‘Public corporations’ peaked in 2014, however the quality of this investment is in question due to the risks of ‘state capture’ in Eskom and Transnet. Incredibly, total public investment in 2022 is lower than it was in the 1970s.

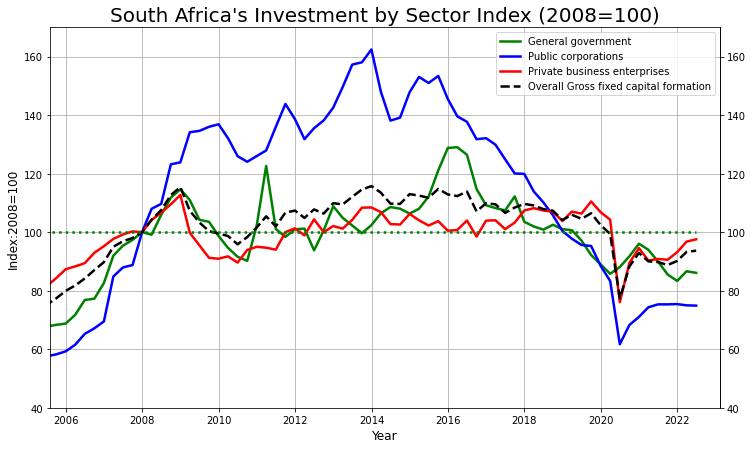

The trend of real investment by sector shows that all sectors have seen a decline in investment since 2008, however private investment is the closest to recovering. While public corporations saw the largest increase but has since declined since the peak in 2014.

Future investment

The overall story of South Africa’s investment is largely negative, with declines in every sector and industry. While a large amount of the ‘public corporations’ investment was possibly of a poor quality. Furthermore, higher future interest rates will likely reduce investment in residential buildings. This declining investment limits the future growth potential of South Africa’s economy.

There is hope however for the future. The changing nature of electricity technology, especially in solar, makes private investment in energy more viable. While there could be a substantial increase in overall investment in electricity as South Africa transitions to more renewable energy, with external funding provided in the COP26 agreement. High commodity prices could also drive mining investment.

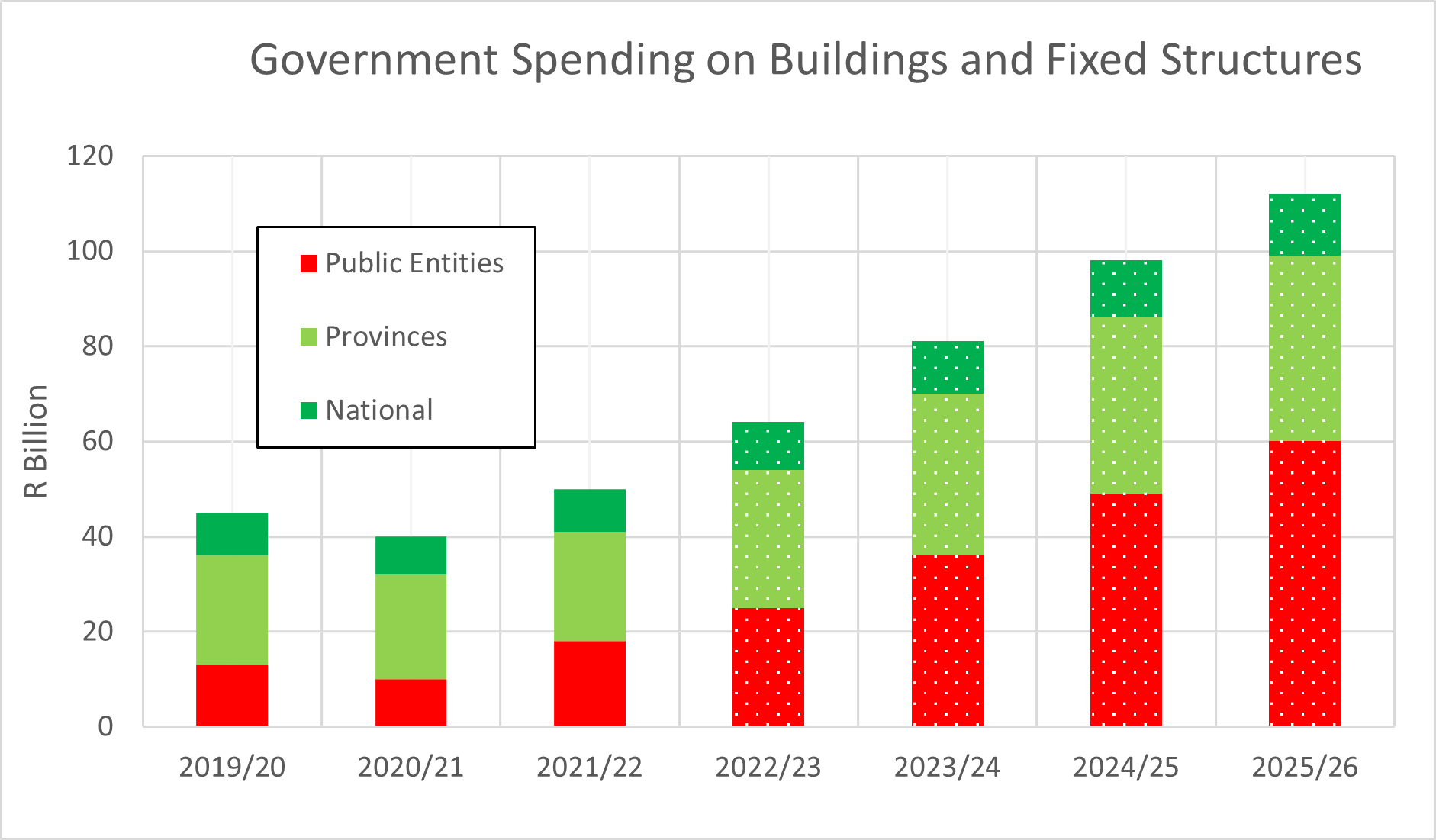

South Africa’s national treasury in the most recent Medium Term Budget Policy Statement has made a commitment to increase public capital investment in the ‘medium term’. This increase is shown in the chart below.

The increase in investment would mostly be focused on roads, railways, and water infrastructure. Note that these planned values are in nominal terms, however it does appear to be a genuine real increase above inflation. While this planned increase in public investment could change, there is genuine hope that the current trend of South Africa’s declining investments could reverse.

“Net investment” is the sum of gross fixed capital formation and change in inventories and is a proxy for yearly investment.