South Africa’s Public Debt

South Africa’s Public Debt

South Africa’s public debt has risen to an unprecedented level. Is it sustainable?

South Africa’s economy is currently really struggling. It has stalled over the past decade and then crashed in 2020. A cloud hanging over it is the rise in public debt. The chart below shows that South Africa’s public debt level has increased to its highest level ever.

Along with rising public debt, global interest rates have started to increase in response to record high levels of inflation. These increased interest rates have reversed international capital flows out of South Africa, resulting in a weaker exchange rate and higher long term debt costs.

Unsurprisingly, the cost of long-term debt and exchange rates move together, driven by international capital flows. There are additional risks associated with a weaker currency: not only does it result in possible increased inflation due to higher costs of imports, but there is also an increased risk of foreign denominated-debt. A high level of foreign-denominated external debt is seen as the “original sin” of emerging markets. The risk is that a currency depreciation would increase the debt levels in domestic currency terms.

The South African Reserve Bank directs monetary policy by changing the overnight central bank rate. Due to a weaker currency and higher inflation — mostly imported through higher energy prices — short-term interest rates have increased. This has resulted in an increase in interest rates throughout the yield curve.

The above graph shows the credit rating of South Africa of the three largest rating agencies. A rating equal to or above BBB-/Baa3 represents an investment grade. Moody’s have rated South Africa at Ba2, while S&P and Fitch have rated South Africa at BB-, both a speculative grade. South Africa is currently at the lowest grade since 1994 for all three of the rating agencies. An increasing debt to GDP ratio, declining credit ratings and increasing interest rates suggests that South Africa is at risk of a sovereign debt default.

The Structure of South Africa’s Public Debt

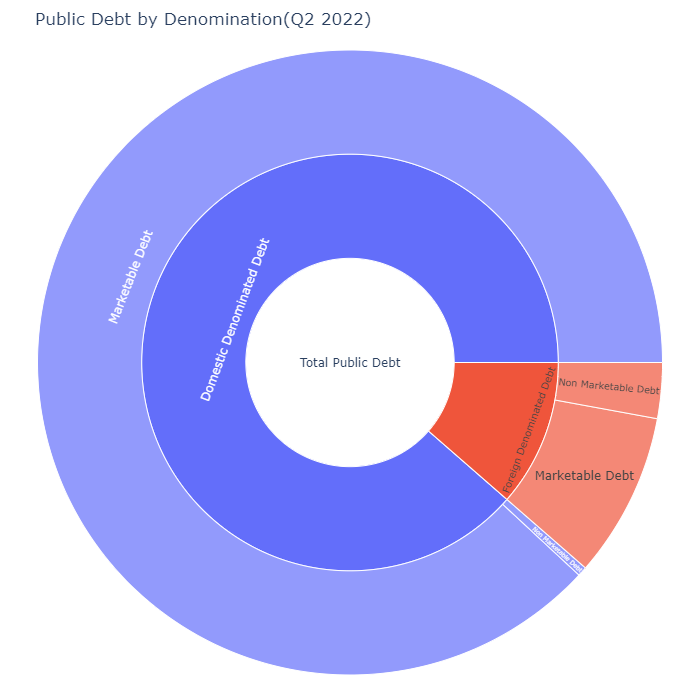

As mentioned, the denomination of debt is important for debt sustainability. South Africa’s public debt, as the pie chart above shows, is mostly in the domestic currency.

However, there has recently been a large increase in non-marketable foreign denominated debt — mostly concessional loans from the World Bank and the IMF. Thus, the total amount of foreign denominated debt continues to increase, even though the overall debt is largely in the domestic currency.

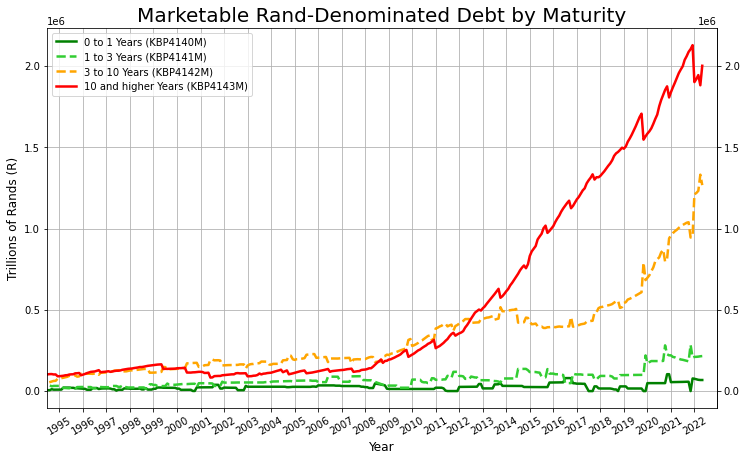

As the above graph shows, South Africa’s debt is mostly of a longer maturity period. This reduces the risk of the weighted debt yield rising rapidly in the event of an economic shock. If necessary, debt of a long maturity is also easier to reduce with inflation. However there has been a recent increase in medium term debt —between 3-10 years — in 2022 of about R300 billion, while very long-term debt has decreased from its peak.

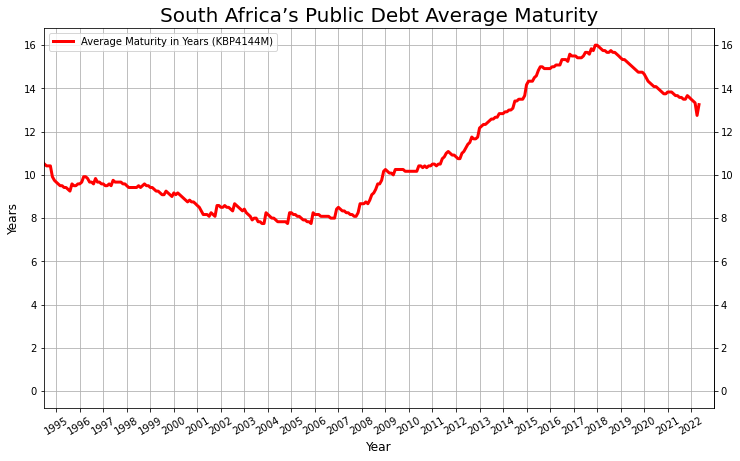

South Africa's average maturity of its public debt is just under 14 years. This has declined from its previous peak of 16 years in 2018. This is still at a high amount; it is much higher than the average of the United States at about five years.

While the marginal cost of debt at various maturities has recently risen, the effective cost of debt — the total interest on public debt divided by the total public debt — has not risen to the same extent. This is due to the relatively long maturity of the debt. South Africa’s effective cost of debt was the lowest in decades in 2021.

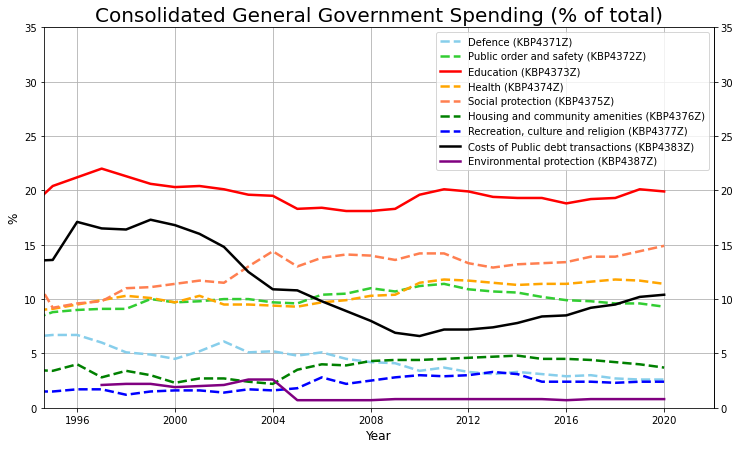

South Africa’s Fiscal Policy

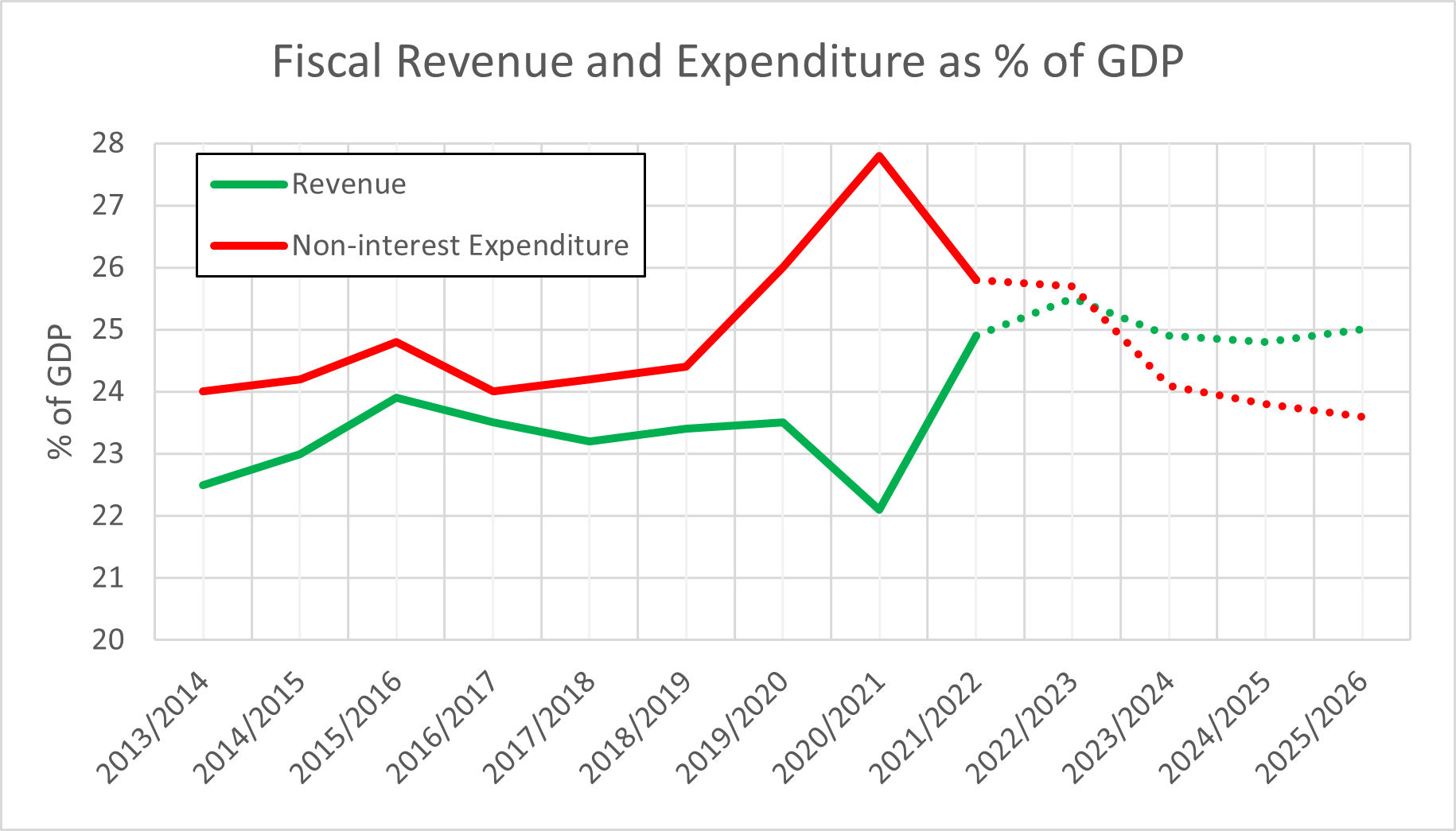

While the effective cost of debt has remained low, the total cost of debt has increased since the low in 2009. As a result of this, South Africa’s National Treasury made the commitment in the 2021 budget review to reduce the fiscal deficit and stabilize the public debt-to-GDP ratio in the 2025/2026 fiscal year. This fiscal consolidation plan would have no tax increases or spending decreases. Instead, inflation was expected to do the work in decreasing real expenditure.

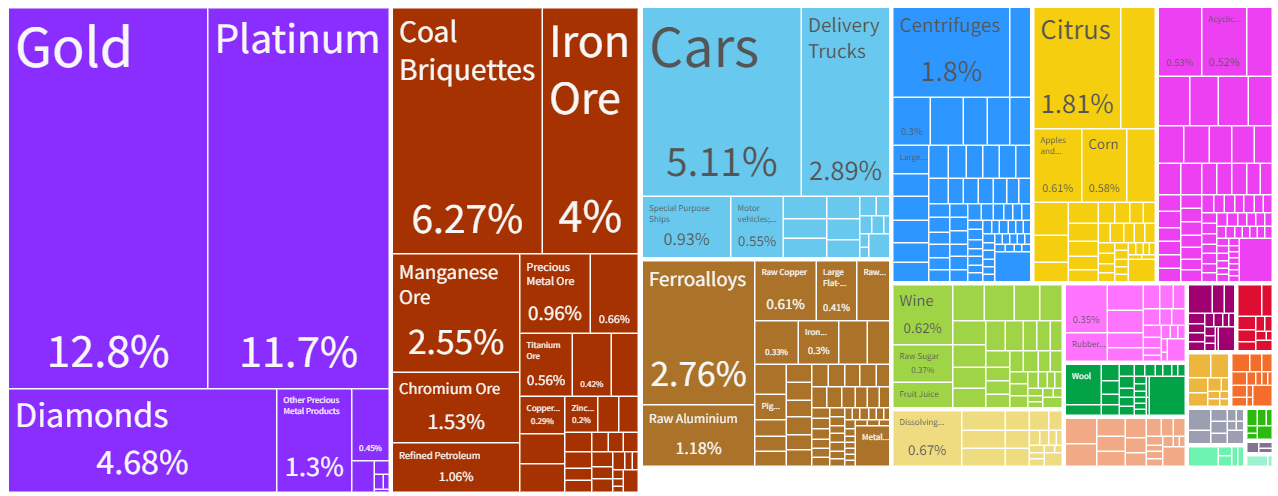

South Africa’s growth prospects have improved since the 2021 budget review was tabled. Increased commodity prices, especially in iron and coal, have supported South Africa’s export revenue. The chart below shows that South Africa is a large commodities exporter.

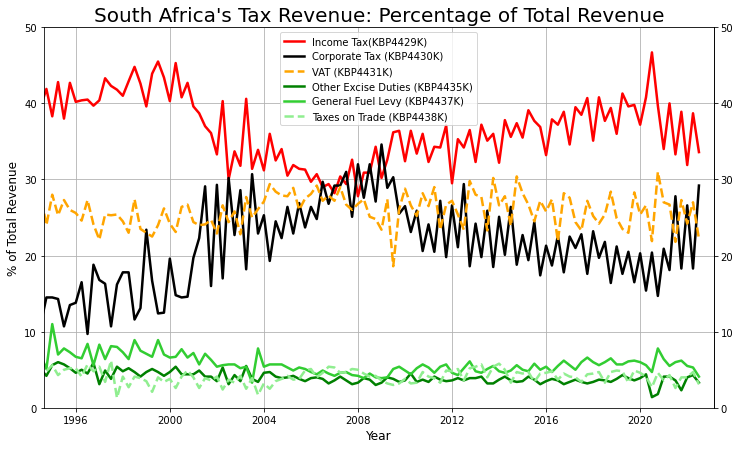

Increased commodities exports combined with an overall economic recovery from the covid-19 recession has resulted in a significant improvement in South Africa’s fiscal revenues. Corporate tax revenue was R105 billion higher and income tax revenue was R37 billion in the 2021/22 fiscal year when compared to the estimates in the 2021 budget review.

In the 2nd quarter of 2022, corporate taxes have replaced VAT as the second most important source of tax revenue. This is likely due to increased profits from mining companies. Corporate taxes were also the primary form of revenue in the late 2000s, the previous commodity boom likely propelled by China’s growth.

The above graph shows that the consumer price inflation has increased after the lows of 2020, with the inflation driven by increase in the price of goods. While the inflation growth for services has been far more limited. This could be a hint that the increase in inflation is driven by supply side factors rather than demand. As a result of increased inflation, South Africa’s nominal GDP has increased to a higher level than expected. South Africa’s National Treasury predicts that a higher-than-normal inflation and nominal growth rate will persist for the next two years.

This higher inflation has supported the National Treasury’s fiscal consolidation strategy — which was based on keeping nominal expenditure relatively constant, while real expenditure would decline. A constant nominal expenditure hasn’t entirely been the case, as there has been increased wages and “additional resources to support low-income households”. The National Treasury is predicting fiscal revenue to be greater than non-interest expenditure in 2024.

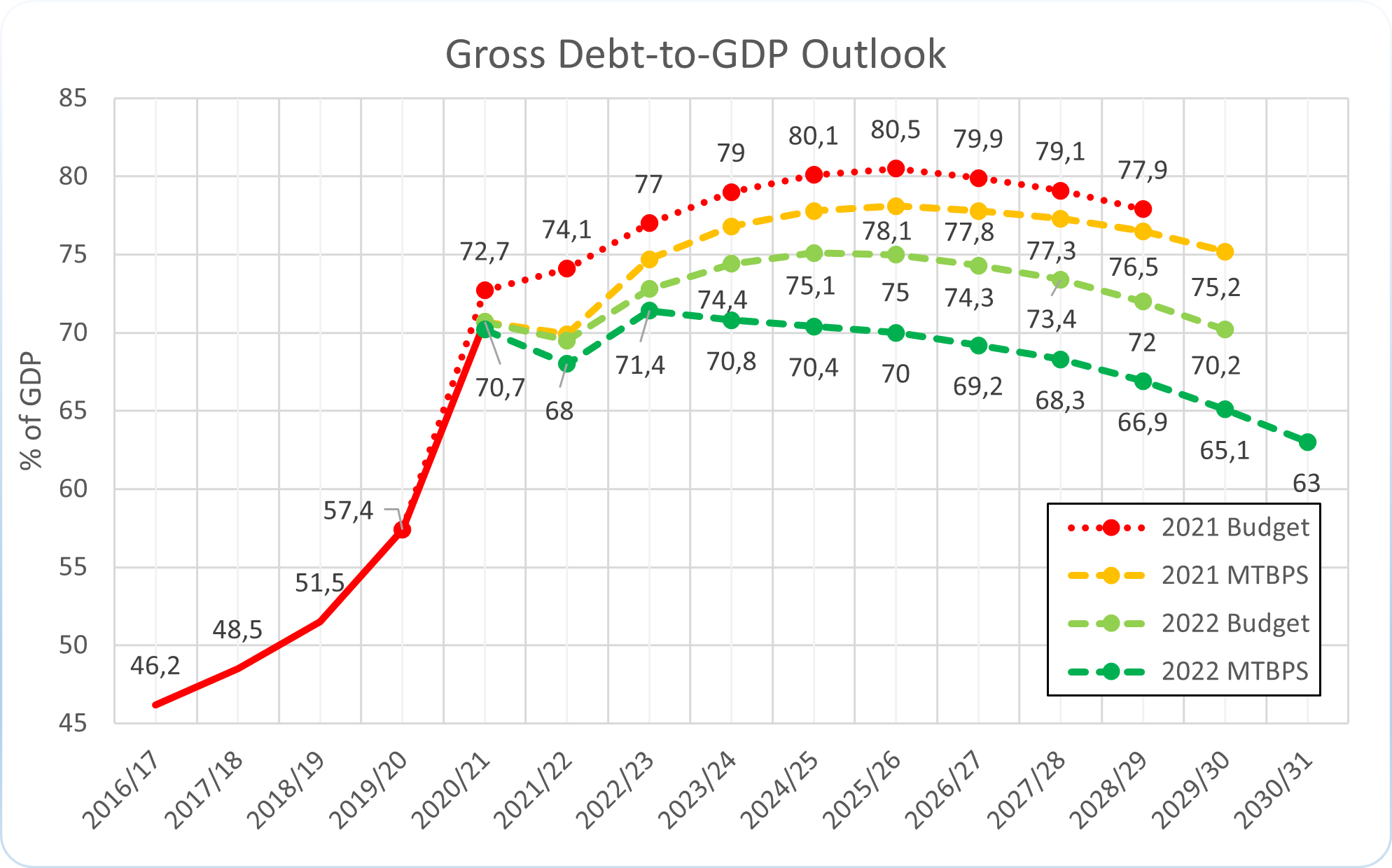

As a result of both higher nominal GDP growth and increased revenue, South Africa’s gross debt-to-GDP ratio is expected to peak at 71.1% in the 2022/23 fiscal year. This is three years earlier and at a lower level than predicted in the 2021 budget review and the 2021 MTBPS. Increased commodity prices and higher inflation were vital for limiting the increase in public debt in terms of GDP, something South Africa’s National Treasury recognizes:

“The improvement in the pace of debt stabilization is largely a result of higher-than-anticipated inflation and revenue.” (2022 MTBPS p.2)

“Over the past two years, South Africa’s broad recovery from the COVID-19- induced crisis of 2020 was supported by higher global commodity prices, which improved export and fiscal revenues” (2022 MTBPS p.3)

The relatively high maturity of South Africa’s public debt was essential in ensuring that higher inflation reduced the real value of public debt. It was prudent of South Africa’s National Treasury to focus the structure of public debt based on a longer maturity and rand denomination. Even though borrowing at a shorter maturity and in US dollars would mean lower interest costs. If that were the case, then the current weaker currency and higher marginal cost of debt would have likely seen a higher debt-to-GDP ratio.

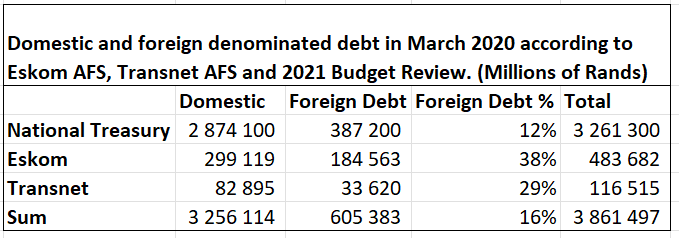

There are several risks to the forecast for the path of public debt. The current commodity boom, like the previous before it, is likely temporary. There is also pressure for increased social spending, public-service wages and support for state owned enterprises. The most recent MTBPS includes a mention of how the government plans to take over a portion of Eskom’s debt. This is concerning as Eskom’s debt has a higher percentage of foreign denominated debt when compared to that of National Treasury, as shown in the table below. However not to the degree that it would derail National Treasury’s fiscal consolidation plan.