Ideas and Economic Growth

Ideas and Economic Growth

I review some of the ideas of Paul Romer; the 2018 winner of the Nobel prize in Economics.

Paul Romer, the winner of the 2018 Nobel Prize in Economics, introduced the concept of ‘endogenous growth theory’, which highlights the role of ideas in promoting economic growth. This theory builds on earlier work called the Solow-Swan growth model — a form of an exogenous growth model.

In the Solow-Swan model, production requires capital, labour and ideas. In this model, the amount capital is dependent on the savings rate, and the amount of labour is dependent on the population growth rate. While ideas are outside the model—hence the term “exogenous”.

In the post about the Soviet Union, I focused on how increases in capital can drive economic growth. Capital however has diminishing returns — there are only so many houses and bridges that one can build. Using the Solow-Swan model on two hundred years of economic data, shows that most economic growth was driven by ideas. Ideas are incredibly valuable; and the potential of ideas is almost infinite.

Convergence

There are two implications of ideas being outside the model: Firstly, there would be overall diminishing returns to economic growth, meaning that rich countries would slow down in terms of growth. Another implication was that there would be convergence — poor countries would catch up with rich ones.

These two things have not really transpired over the last century. Firstly, the growth of the richest and most productive country in the world — the United States — has remained remarkably consistent over the past century, at roughly 1,1% per capita growth per year. This is the first time in human history that this has been the case for so long. There has also not been any convergence — the gap between the US and Africa and South America is the furthest it has ever been. Parts of Asia and Eastern Europe have caught up, but the world is far from converging to US levels of economic prosperity.

Ideas as a recipe

One reason why the world is not converging, and the US continues to rapidly grow is the role of ideas in economic growth. Ideas are important — they should not be seen as an exogenous factor in growth, but at the core of it. Romer—given his physics background and thinking of the law of conservation of mass —understood ideas not as a form of production, but instead as a way to rearrange things. Nothing new is ever being created, instead new things are best understood as a rearrangement of existing matter—new combinations of existing things. Ideas are instead a recipe, a formula or blueprint for making new things. Think of a master chef creating a meal using simple ingredients. It is often the recipe and method, rather than the ingredients, that make good chefs so valuable.

The nature of ideas

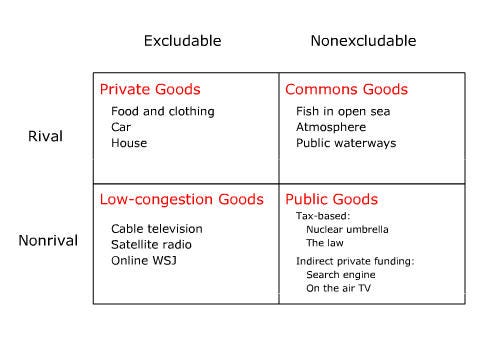

Ideas differ from a standard product. One reason is that it is more similar to what economists call a public good, making it harder for the private sector to invest in it. The two things that make a public good are nonrivalry —there is an unlimited supply, and non-excludability — it is not possible to exclude others from using it.

Ideas are clearly nonrival—once a recipe is created, it can be copied with little cost.

“Ideas are not depleted by use, and it is technologically feasible for any number of people to use an idea simultaneously once it has been invented” (Charles I. Jones p.860)

It is also hard to exclude others from using an idea once it is out in the open. The risk of this is that creates a ‘free-rider problem’ for those who want to profit from ideas, which reduces the incentives to invest. It is possible to create property rights around ideas, such as patents and copyrights. Institutions such as a legal system and ‘rule of law’ are also required to protect these property rights. With the right institutions, it is possible to create clear incentives to invest in ideas. This can be incredibly valuable.

Apple Computer — Why ideas are so valuable.

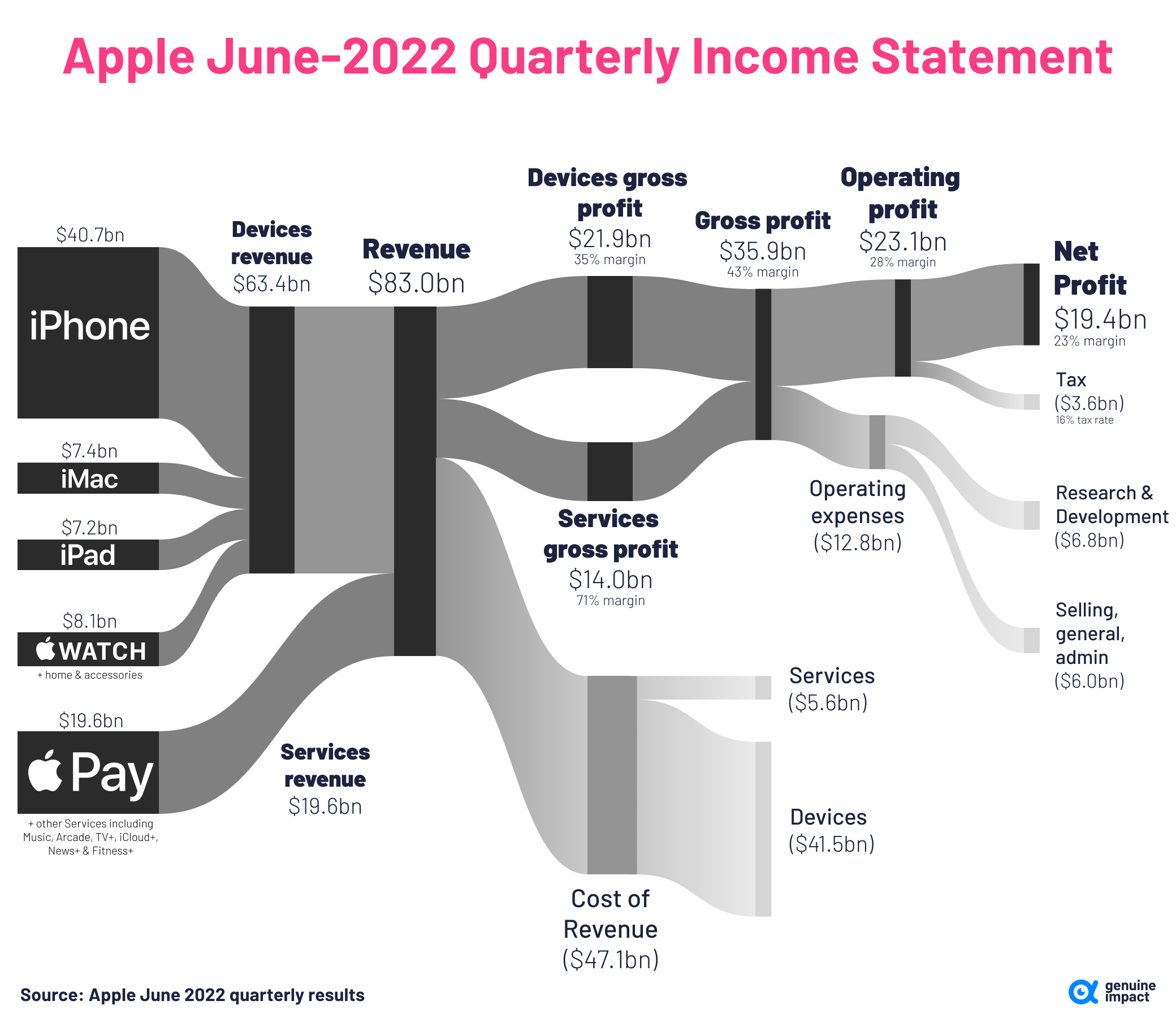

An example of the value of ideas and the institutions surrounding it is the value of Apple Inc., the most valuable company in the world in terms of market capitalisation. Most of Apple’s revenue comes from the production of the iPhone, other computer products and online services.

Apple however doesn’t physically make anything. Instead, it outsources most of the production process to two Taiwanese companies: TSMC — the maker of computer chips, and Foxconn — a manufacturer with most of its factories in China. Apple does however own the patents to the design of its phones and the software in it. It is the brand and designs of Apple — legally protected with patents — not its raw materials, that makes it the most valuable company in the world. Hence the focus on the mark “designed by Apple in California”.

Property Rights

There are however risks to property rights around ideas being too strong. You would want some sort of patent system to encourage investment in new ideas. The prospect for an inventor to become rich is a powerful incentive.

However, you would not want property rights it to be too strong. Ideas tend to build on each other — Newton said that he “stood on the shoulders of giants”. Thus, the discovery of new ideas requires that ideas be spread out. Ideas are better when more people have them, as it increases the chance of discovery. Therefore, there are increasing returns to scale with ideas, the opposite of capital. It is this increasing returns to scale in ideas, that has driven economic growth.

How does the nonrivalry of ideas explain economic growth? The key is that nonrivalry gives rise to increasing returns to scale. (Charles I. Jones p861)

The value of reducing property rights for ideas is especially true when ideas have very high positive externalities, such as a vaccine. However, the risk of removing patents is to discourage future investment. It is therefore better to have some sort of mixed system with ideas having property rights and being spread freely.

Divergence

Given the low cost of copying ideas, its nature as a recipe and economies of scale —means that there is almost infinite potential for growth. This infinite potential of ideas has very different implications that better explain the world when compared to the narrower Solow model. It better explains why there has been a lack of convergence in standards of living between countries. Some of the policies that help to foster the creation of new ideas include investments in research and development, human capital and intellectual property rights. Rich countries are good at doing these things which, according to Romer’s model, drives their growth and divergence.

The United States is very good at creating new ideas: it has the world’s best research universities, and it is incredibly good at creating and attracting smart people from all over the world. Overall research and development spending in the US is the highest in the world and one of the highest in terms of percentage of GDP. The US also has a large and educated population, allowing for greater specialisation and a larger pool of workers to focus on research.

“Just as more workers produce more cars, more researchers generate more ideas” (Charles I. Jones p878)

Workers outside of researchers also play a role in generating new ideas. As mentioned in the post about Schumpeter, entrepreneurs creating new ideas and a competitive market to test these ideas are vital for “creative destruction”. The Soviet Union invested large amounts in research and human capital, these were not good outside of space and military technology — the industries in which the Soviet Union had clear international competitive pressures. Competition is vital to test ideas. Think of the music industry and all of its creativity and innovation. If all music came from music professors or music students, the overall quality of songs would be far lower. That’s because academic output is often not put to the test of market pressure.

The Future

While the potential for ideas is infinite, there is some evidence of diminishing returns to ideas. In the book “Human Frontiers”, Michael Bhaskar puts forward the theory that we have hit the limits in our ability to generate new ideas. This is evident in Eroom’s law:

“Eroom’s law: The number of drugs approved for every billion dollars’ worth of research and development halves every nine years” (Human Frontiers p.55)

There is evidence of Eroom’s law in other sectors:

“The typical estimate in Bloom et al. (2019) suggests that research productivity declines at a rate of about 5 percent per year, meaning that the level of research productivity falls by half every 12 years.” (Charles I. Jones p.874)

The concern is that the ‘low-hanging fruit’ of ideas have already been found, leaving ideas that are harder to obtain. The number of resources spent to generate ideas has grown exponentially over time — there are more scientists than ever before — while the growth rate of productivity, a proxy for technology, has remained relatively stable.

There is hope for the future. The developments in AI models, such as OpenAI’s ChatGPT, hints at a new productivity boom. Developments in health, such as the mRNA vaccines, could help to extend human life. The first person making it to 150 has likely already been born. The improvements in renewable energy and battery technology could herald an age of genuinely abundant electricity. We are potentially on the cusp of an age in which standards of living could dramatically increase, driven by the creation of new knowledge and ideas.