Demographics and Interest Rates

Demographics and Interest Rates

The world is rapidly aging, this has a greater effect on the macroeconomy than most realise.

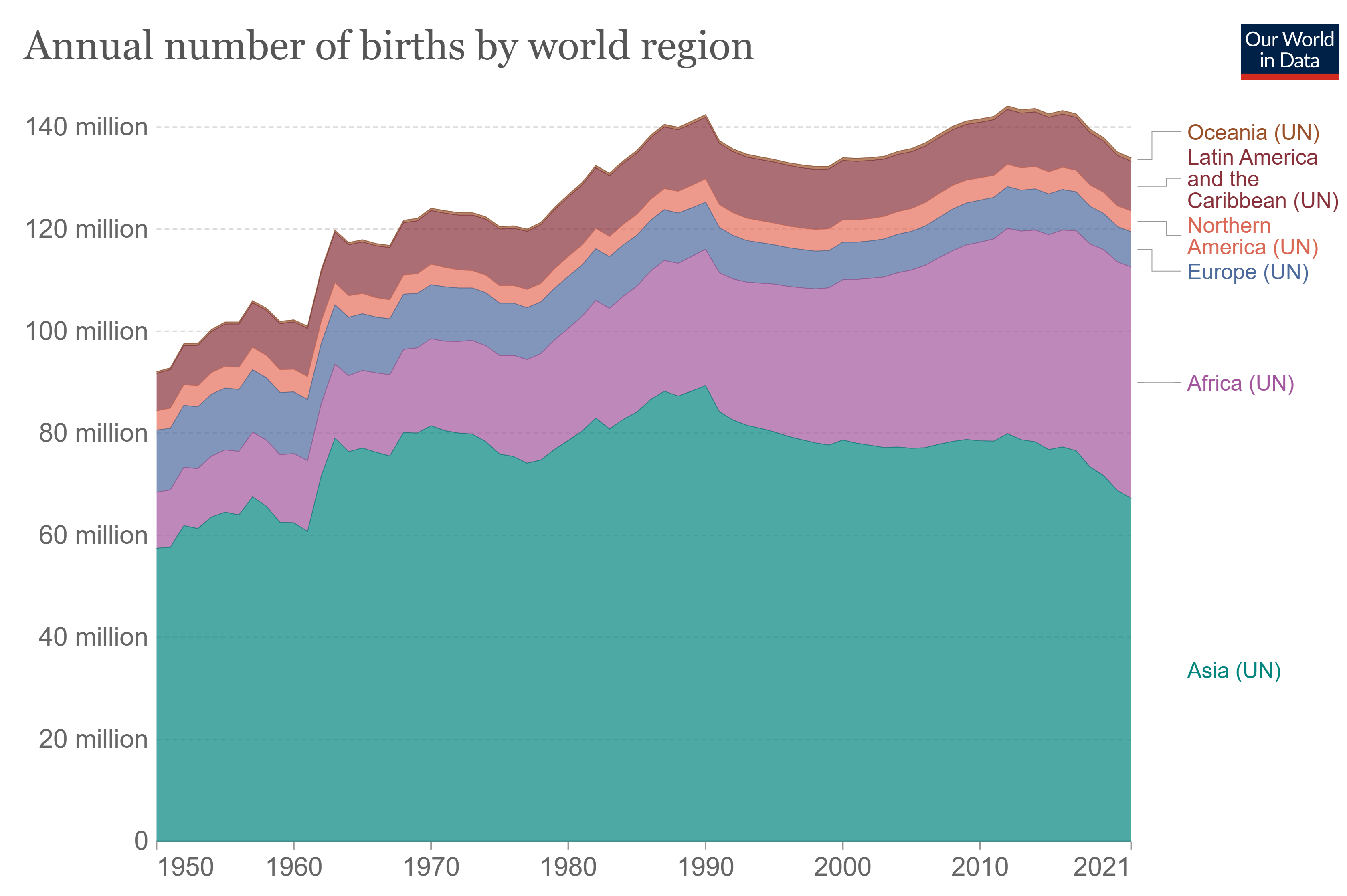

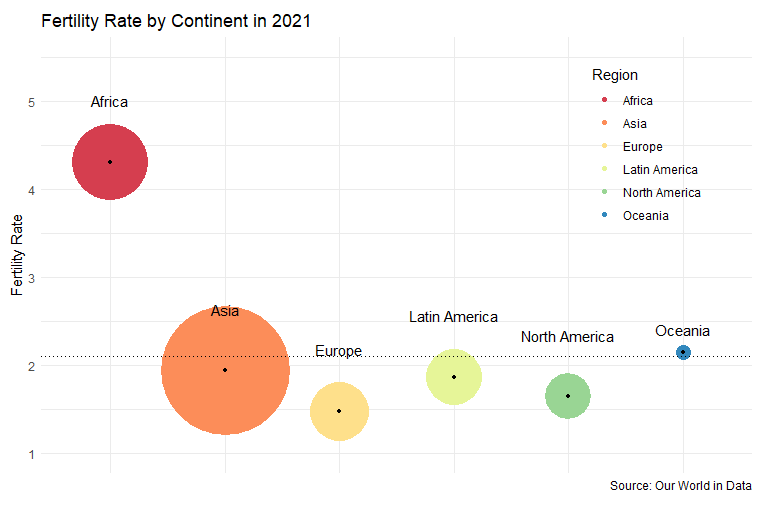

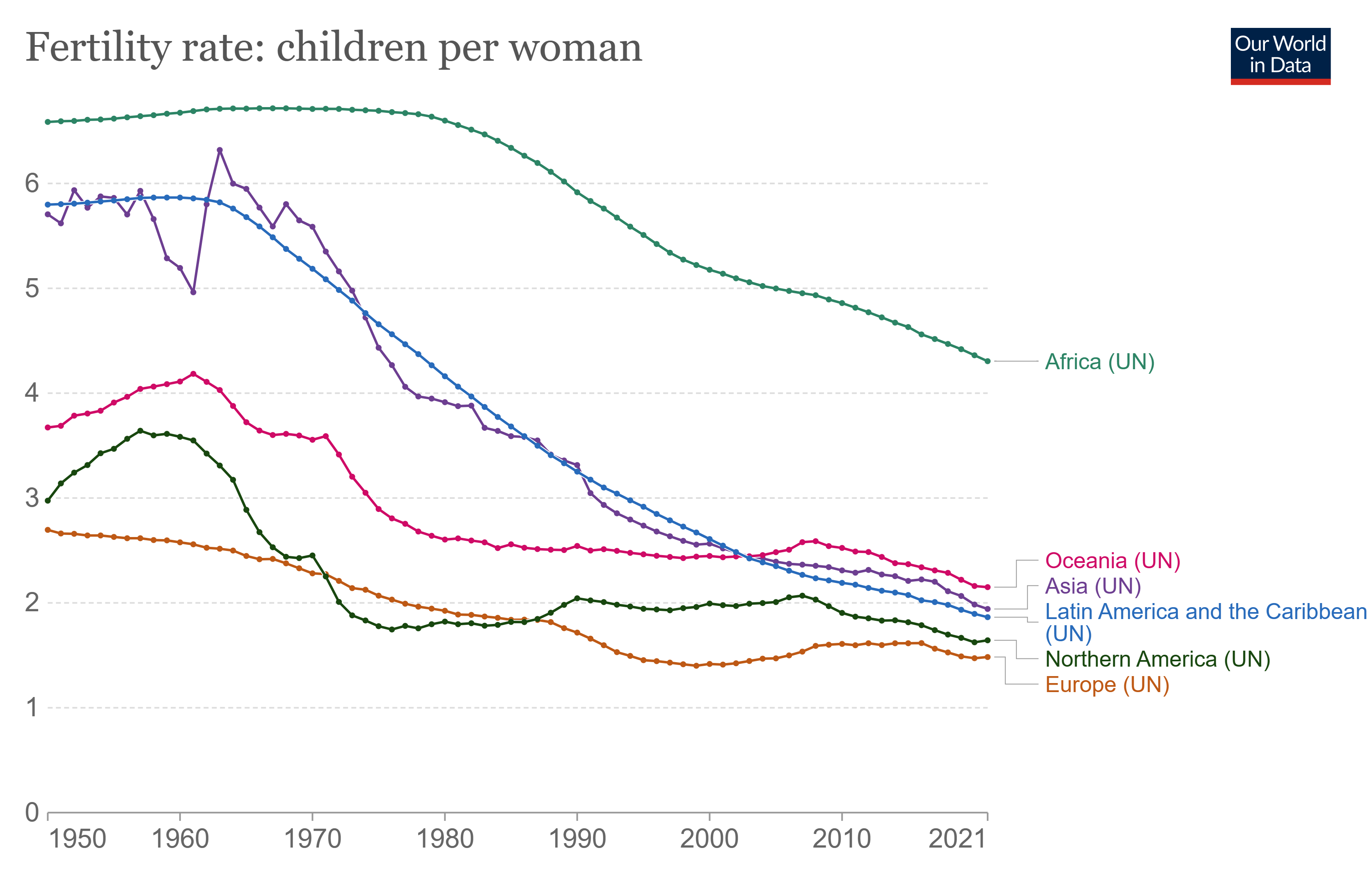

The world is rapidly aging and the total number of births each year is declining, with the decline being more evident in the rich world. Every continent in the world, except for Africa and the tiny Oceania, has an average fertility rate of less than 2. A fertility rate below 2 is typically associated with declining population size over time. Countries with low fertility rates may face challenges related to an aging population and a shrinking workforce, as well as potential strains on social security systems and other public services.

As a result of this low fertility and decline in total births, combined with improvements in health and technology, average ages have increased in almost every country.

This increase in average age likely has had macroeconomic effects, including on interest rates. Interest rates are, in many ways, determined by the balance between savings and investments. Higher levels of investment tend to raise interest rates, while increased savings can reduce them. The day-to-day and other cyclical fluctuations in interest rates are influenced by monetary policy and risk sentiment.

Aging and Interest Rates

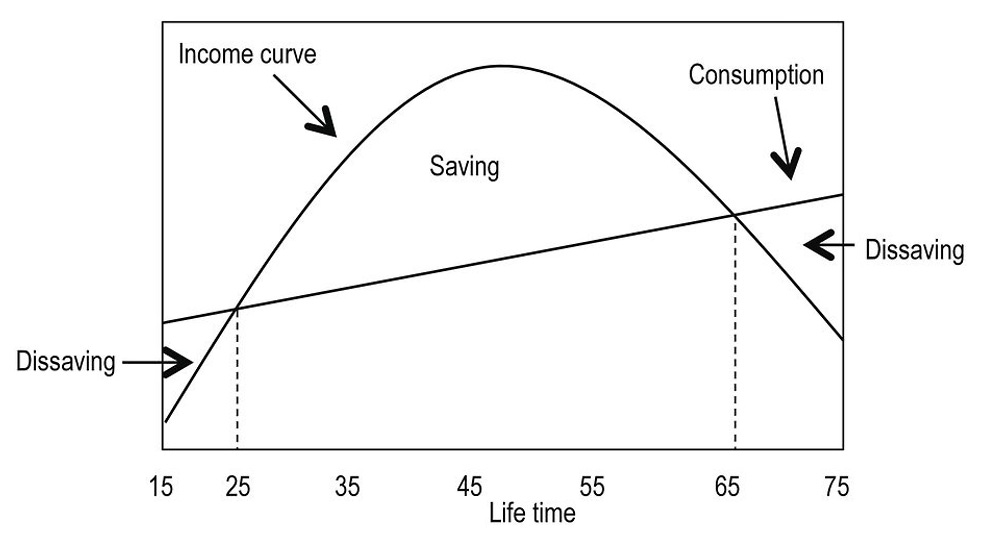

There are multiple ways in which demographics can affect interest rates. One interpretation is the life cycle hypothesis by Franco Modigliani and Alberto Ando which states that individuals smooth their consumption over their lifetimes, thus saving in periods of high income and borrowing in periods of low income. This suggests that the stock of savings will build up during working age and peak at retirement, then decline after. In other words, wealth accumulates over time as individuals get older. This can be aggregated to entire countries, thus countries with an older average age have a larger pool of savings. This does not last though. As the average age moves beyond retirement age, the life cycle hypothesis suggests that the pool of savings declines and government borrowing costs potentially increase. However, the desire to save increases as health and life expectancy have increased over time, limiting the retirement effect of the decline in savings. A shift to a more information intensive economy has also increased working lives — look at the age of Joe Biden or Warren Buffet — and increased the effective retirement age.

Another interpretation is that raising children can be expensive, resulting in households with few or no children being able to save more. A third interpretation is more forward-looking, suggesting that low fertility and an aging population are likely to reduce future population growth rates, which, in turn, may reduce future economic growth rates. This lower expected growth could reduce investment, resulting in lower interest rates.

There is a clear decline in fertility rates resulting in declining populations in many countries’ younger generations. Japan is the furthest ahead in the demographic transition — which has possibly resulted in persistent deflation and very low interest rates. Japan reveals the future of many advanced economies, in which the decline in the growth rate of the population partly results in a decline in interest rates because of increased savings and declining investments. According to Etienne Gagnon and others, advanced economies have reached a “new normal” of “low interest rates, low output growth, and low investment rates”.

Government policy have also played a role in driving down interest rates. After the 1997 Asian financial crisis, many countries bult up foreign exchange reserves. Mercantilist trade polices also played a role, with many countries accumulating reserves to weaken currencies and promote trade surpluses.

Dan Alpert suggests that this ‘excess savings’ in Asia and in other rich countries combined with a US government fiscal surplus in the early 2000s created a ‘global save asset shortage’. This shortage incentivised private sector financial speculation and indirectly caused the 2007-2008 financial crisis.

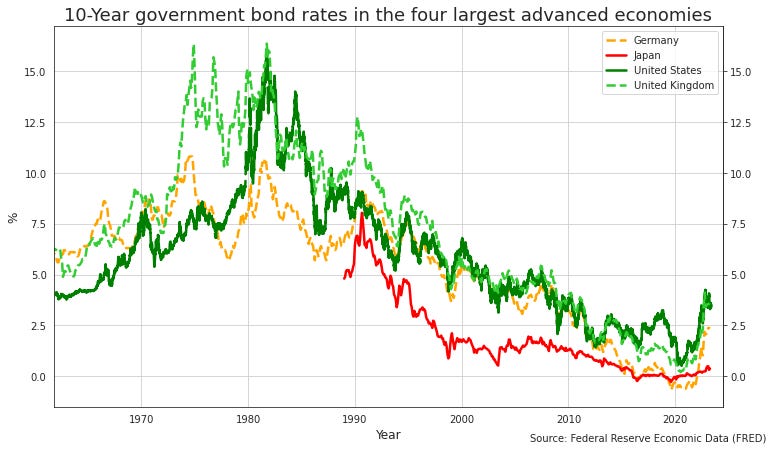

Secular Decline

The graph above shows the decline in interest rates proxied by the 10-year government bond rate of the four largest advanced economies. High interest rates during the episodes of the 1970s and 80s were driven by high inflation, which changed after the “Volcker shock” in the 1980s. Since then, most developed countries have mostly avoided high levels of inflation. There are several other factors driving down interest rates and inflation in the last few decades, including improvements in technology reducing energy and supply costs, increased trade and financial flows and the shift of supply chains to cheaper emerging economies. However, some of these factors have reversed in the past two years, leading to an increase in interest rates and inflation.

Other views from Larry Summers, Tyler Cowen and Robert Gordon see the decline of interest rates and inflation due to “secular stagnation” in which the decline in technology breakthroughs — and other factors — leads to weak long-term growth prospects and lower interest rates. The rise of less capital-intensive information technology has also possibly played the role, reducing the need for large capital investments. Others such as Stephanie Lo and Kenneth Rogoff see it as the result of deleveraging after the financial crisis. Atif Mian and others suggest that declining interest rates are driven by rising income inequality, increasing the savings of the highest earners.

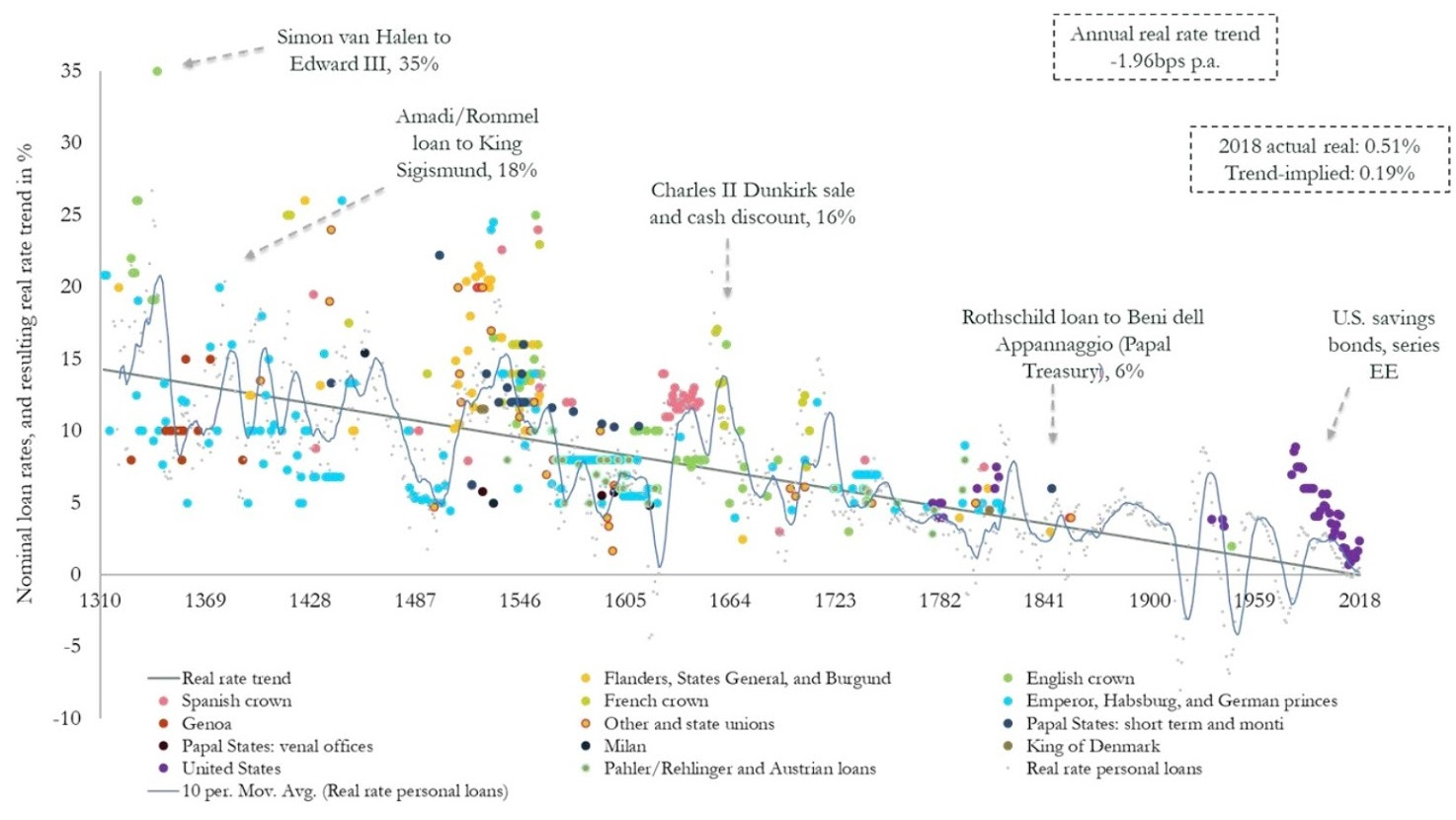

This general decline in interest rates over the last few decades is not new. Paul Schmelzing reconstructed real interest rates from 1311 to 2018 in multiple assets classes and found a “persistent downward trend over the past five centuries”, except for the relatively brief periods of 1550-1640, 1820-1850 and 1950-1980. One possible explanation for this trend may be increased “capital accumulation” or accumulated savings over time. Schmelzing concludes that the current negative “sovereign” real interest rates in advanced economies are in line with the “historical trend” and have entered a “permanently negative territory”.

Effects of declining interest rates

The effects of this general decline in interest rates are multiple and interest rates and assets prices are inversely related. Thus, lower interest rates have likely caused assets prices — such as stocks and housing in the rich world — to rise to higher levels than ever before. A form of ‘asset price inflation’. Lower rates also support increased government borrowing, which is now at the highest levels ever. Public debt in Japan – the country the furthest along the demographic transition – is over 260% of GDP.

Demographics and Interest Rates in Africa

Many parts of Africa and other developing countries have the opposite problem. As pointed out by Charlie Robertson, Africa’s fertility rates are high, families are large, and average ages are low. This has resulted in low amount of accumulated savings and a limited pool of savings for governments and industry to borrow from. If African firms and governments do want to invest, they have to rely on either external debt in a foreign currency — which has its own risks — or on foreign ownership, which possibly weakens the incentive for property rights. Thus, high fertility rates can potentially limit savings, investment, and economic growth.

The future

The exact trend of future interest rates is hard to predict. As the world has seen in the past two years, there are many other factors — such as disruptions in energy, trade, and fiscal policy — that could influence interest rates and inflation. Another is the role of technology, recent improvements in technology could drive growth and investment, resulting in higher interest rates. One more reason is a greater willingness of governments in rich countries to spend and invest. However, the effect of demographics on savings is unlikely to change. Changes in demographics tend to be very slow, and a reversal of the current trend of increased aging is unlikely. Overall, I don’t think that there will be a significant change in the role of demographics in driving up accumulated savings and lowering interest rates.